Enterprise Retail Merchants: Combine Universal Solutions, Data Ownership and Speed to Market To Optimize Payment Outcomes.

Payment innovation is accelerating, and retailers need to keep pace to stay competitive.

While payment trends among retail merchants vary by region, sub-vertical, and size, several common elements resonate across any merchant accepting card payments. Considering that 77% of in-person purchases and 89% of online payments are made by card, these apply to most merchants. Focusing on security, fraud prevention, and seamless customer experiences is critical for long-term success. Equally important is how quickly and efficiently merchants can adapt to and accomplish these priorities.

Security and Fraud Prevention

As merchants expand to innovative payments to attract more customers, protecting their underlying payment infrastructure is even more vital. While contextual commerce in digital, mobile, and social commerce channels reduces purchase friction, it can also create more security risks and potential for fraud, identity theft, and other malicious criminal activities. Credit card fraud was the most common type of identity theft in the first half of 2024 in the US. Fraud in Card-Not-Present (CNP) transactions, where our enterprise retail merchants get a significant portion of their business, is expected to be responsible for 74% of card payment fraud loss in 2024.

Credit card fraud has evolved over counterfeiting, stealing, phishing, and hacking. Fraudsters turn to online payments as protections like EMV chips are introduced for Card-Present (CP) transactions.

Tokenization - which replaces raw information with randomized digits of the same length and format - ensures that sensitive card data used for online purchases can be held securely without risking a breach.

The benefits of tokenization have resulted in tokens proliferating across the payments ecosystem in a layer cake of processor tokens, network tokens, device-specific tokens such as from Apple Pay, and new merchant-specific tokens - to the extent that many times, multiple tokens support one transaction to keep it secure.

Embedded Payments

A technology is successful when it moves from innovation to invisibility - as a seamless part of the customer experience. Embedded payments, projected to grow by 300% and cross $138 Billion by 2026, are becoming a cornerstone of many enterprise retail merchant experiences. Whether it's the embedded payment in a gig platform, a saved credit card on an e-commerce website or an app, an offer for insurance when buying travel, buying a product on an Instagram feed, or paying for upgrades within your car's software-enabled ecosystem, embedded payments allow customers to focus on their purchase and can result in up to 98% retention rates for embedded payments.

Anglela Strange from a16z famously said, "Every company will be a fintech company." Retailers looking to boost incremental revenue through embedded payments should consider expanding their online or mobile presence based on a best-of-breed provider. Engaging vendors that offer processing redundancy, enable PSP orchestration, and reduce PCI compliance would ensure a future-proof solution.

Next-Gen Experiences with New Technologies

When consumer payment preferences evolve, retailers need to adapt quickly. AmazonGo in the US and 7-Eleven Shop and Go in Singapore offer cashierless purchases and are on the rise, and 97 million (34% of total) Americans in 2024 already use BOPIS (Buy Online Pay in Store) regularly. Tap to Pay is projected to grow by 150% by 2028. Up to 49% of Americans have used BNPL as of 2024, and Pay By Bank is expected to grow substantially in the US to catch up with India, Brazil, and China.

Legacy systems, protracted implementations, and unwieldy payment infrastructure add time and effort and hamper the quick adoption of emerging technologies. These issues are multiplied for large merchants who have added PSPs, processors, and gateways to add coverage and redundancy but now need to manage data and map to a single value across them all. A single product layer that supports ease of integration by being API-first and functions as a unified interface to manage multiple payment methods can make it easier for merchants to roll out cutting-edge experiences.

A Solution to Stay Ahead

VGS has worked with leading retail merchants as an enterprise payments platform for years to successfully address several concerns most merchants share and deliver solutions.

- Payment Stack Optimization

- Maximize Authorization Rates and Cost Efficiency

- Shorten Time to Market

- Super-Charge Marketing and Loyalty Programs

Payment Stack Optimization

Unifying payment collection for any payment method in a single location and operating seamlessly across PSPs while maintaining PCI compliance are priorities for most established merchants.

Customer: Global Restaurant Chain

- An enterprise merchant had corporate-owned and franchise operations, but there wasn't a central system of record to track payments across varied providers for the company and franchisees.

- The fragmentation resulted in an inconsistent user experience across payment methods and locations and hampered their objective of achieving digital parity.

VGS Solution: Central Payments Hub and Universal Payment Collection

- Working with VGS, the merchant could achieve an interoperable payment layer across all their operations that bridged the gap across online, in-store and cross-franchisee PSPs, internal payment logic, and PCI compliance postures.

- VGS offered universal payment collection by tying each payment credential, whether used on web checkout, in-app or via API, to a single aliased token.

- The merchant finally achieved a centralized hub across providers to enable a uniform experience across payment methods, transaction types, use cases, and locations.

Maximize Authorization Rates and Cost Efficiency

Efforts to raise authorization rates get diluted when multiple providers, outdated infrastructure, and proprietary systems interfere. Merchants' payment outcomes can be impacted if their ecosystem is fragmented, with multiple PSPs, processors, gateways, and vendors that can't easily connect with other providers.

Customer: One of the largest SaaS providers

- An enterprise merchant wanted to resolve siloed vaults with individual PSPs to reduce their reliance on PSP vaults and their individual processors' connections.

- Any products that optimized authorization rates, such as network tokens and account updaters, had to be purchased individually from each PSP, and the resultant data had to be reconciled across them all.

VGS Solution: Data Centralization and Ownership

- Working with VGS enabled the merchant with a universal token vault to store and secure all their data while managing costs and operations better to limit paying for duplicate vaults and multiple optimization solutions.

- Layering on our neutral network tokenization and account updater solutions, which worked across all their card payment credentials and not just a portion, enabled them to increase authorization rates and reduce fraud by replacing millions of PANs with network tokens and keeping card credentials up-to-date with the latest information.

- Moving to a central external vault freed them from PSP limitations and work with any vendor they chose.

Shorten Time to Market

Adding new vendors can mean time-consuming and costly implementations and significant changes to your tech stack. The technical overhead burden is substantial enough that many organizations delay payments and treasury modernization efforts, and 88% of CFOs are concerned about successfully capturing value from their technological investments.

Customer: Global creative platform

- An enterprise merchant wanted to improve payment performance with more successful transactions, updated credentials, and deeper card insights.

- Although they identified network tokens, account updaters, and card attribute services as meeting these needs, they were concerned about signing up for multiple, tech-heavy individual integrations that would be drawn out for months and push out ROI.

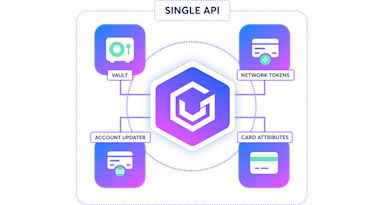

VGS Solution: Card Management Platform

- VGS provided a consolidated card management platform that enabled the merchant to access network tokens, account updater, and card attributes with one API integration for a single endpoint.

- A straightforward integration coupled with an interoperable and composable platform reduced the time needed to get to market by 75%.

- The platform's flexibility meant the merchant could choose the services they needed and select options, such as the frequency of account updates, that met their business needs and supported better cost management.

Super-Charge Marketing and Loyalty Programs

Loyal customers spend 67% more on average than new customers, and 75% of customers would switch brands for a better loyalty program. The stakes are high for merchants to offer market-leading experiences.

Customer: LargeQSR merchant

- An enterprise merchant approached VGS to help deliver a seamless omnichannel experience to their customers.

- Changes in their payment infrastructure meant they had different PSPs for e-commerce and POS transactions in North America and couldn't match a customer's activity across channels.

- This could have severe implications for the loyalty rewards their customers expected and the risk of losing them to the competition.

VGS Solution: Omni-Channel Matching

- VGS centralized the merchant's data across PSPs in its dedicated vault and seamlessly linked payment credentials to map both online and in-store transactions from thousands of stores across multiple countries to an omnichannel alias or token.

- This enabled the merchant to take a unified view of consumer behavior vendors, geographies, and payment channels, eliminate fragmented data issues, and create loyalty offers for targeted customers based on a comprehensive view of their purchasing activity.

- With VGS, the merchant seamlessly integrated consumer purchase data into their Customer Relationship Management system without exposure to sensitive data and maintained PCI compliance.

Optimizing your payments stack requires a focus on data centralization, improved payment outcomes, and faster time to market while delivering seamless user experiences.

We've helped leading merchants achieve this and more, with the added benefit of working with a single, vetted vendor.

Are you curious to know how others have future-proofed their payment stack?

Let's connect to discuss how VGS can enhance your payment infrastructure with universal solutions that combine cost efficiency, scalability, and speed.