Combining these ensures a robust payment infrastructure that increases authorization rates, reduces costs, maximizes coverage, and retains access to the PAN.

Merchants face various payment challenges, from duplicate vendor fees to fraudulent activity, yet one objective remains constant: driving authorization rates. In this article, we discuss how combining two key technologies, Network Tokens and Account Updater, can help retailers manage payment complexities, while optimizing payment processing securely and efficiently.

According to the Merchant Risk Council (MRC), high processing fees, poor customer conversion, and increasing risks of chargebacks and fraud are among the top 5 issues in accepting card payments that are top of mind for merchants.

However, merchants know, and Mastercard agrees, that they must also focus on:

- Adapting to technology to meet consumer expectations

- Standardizing systems while accommodating regional preferences

- Enhancing security to fight growing threats

- Ensuring compliance with new regulations like PCI 4.0, mandatory by March 31, 2025

It could be easy to assume that these objectives work independently. For example, lower authorization rates are the price to pay for more robust payment security, adding new payment methods will result in complex compliance requirements, or higher authorization rates can't coexist with lower fraud.

But what if there was a solution that helped merchants accomplish all their objectives:

- Optimal authorization rates

- Better security

- Stronger fraud mitigation

- Higher processing cost efficiency

- PCI compliance

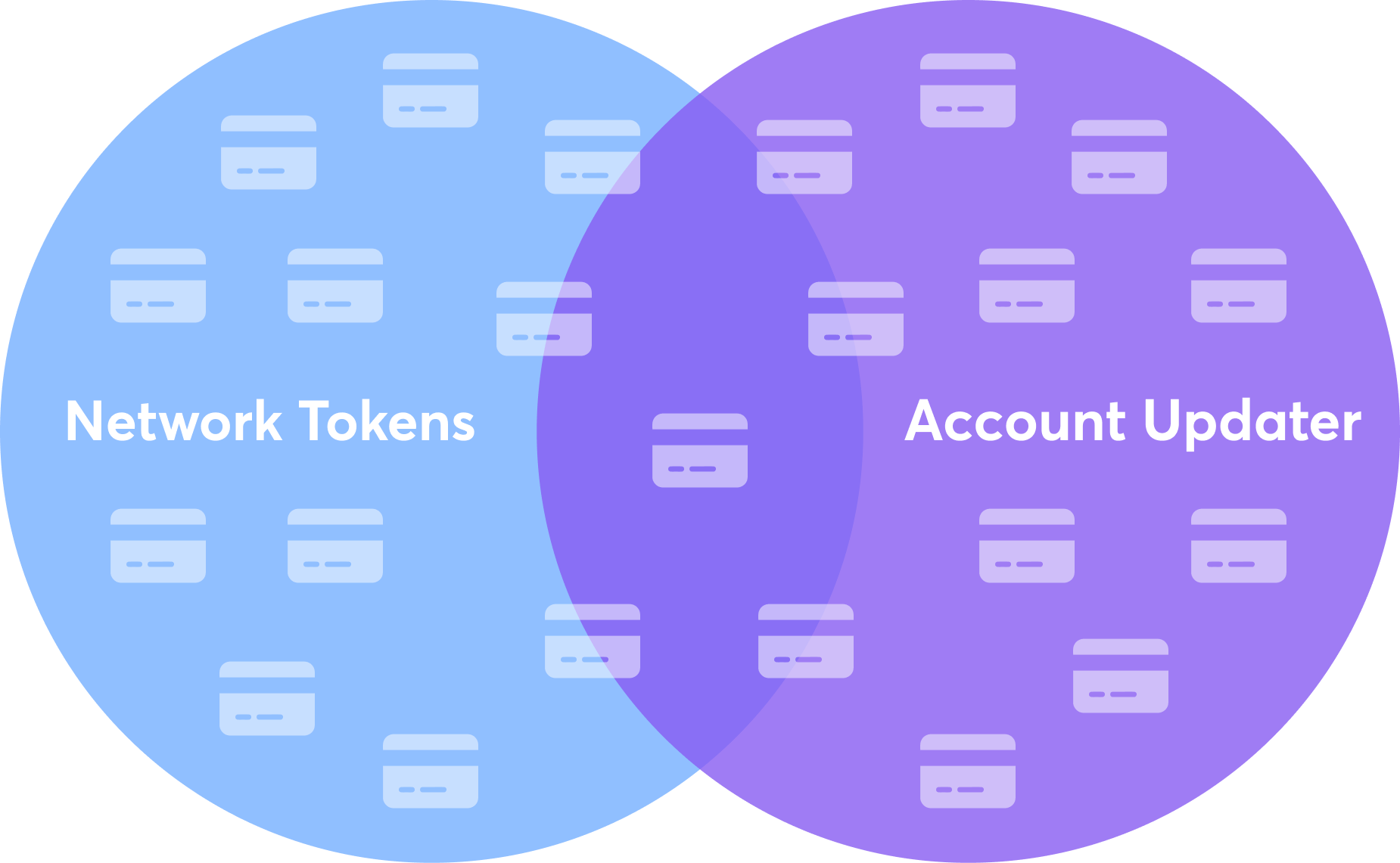

That's where a combination of Network Tokens and Account Updater comes in.

Do I need both Network Tokens and Account Updater?

Yes.

For card coverage, to access both automatic updates and fraud protection, ensure cost efficiency, and retain the flexibility to retry transactions and access additional PAN-specific services like Card Attributes. Best-in-class merchants keep connectivity to the PAN for successful card lifecycle management.

Remember: Not all cards are network token-provisioned, and not all acquirer processors accept network tokens.

Access Network Tokens and Account Updater individually or with a single API integration with the VGS Card Management Platform.

Maximize card coverage with both solutions.

A quick refresher

Network Tokens and Account Updater, along with Card Attributes, enrich your sensitive card data for better payment outcomes, improve your user experience, reduce fraud and lower costs. The data can be securely stored in VGS's independent PCI-compliant vault or another vault associated with your existing systems.

Network Tokens

If a merchant uses network tokens, they have replaced sensitive information like a card number or 16-digit PAN with a non-sensitive 16-digit randomized value. Although it can still be recognized throughout the card payment processing lifecycle, it eliminates the risk of handling raw information. Network tokens are automatically updated to remain current even when the underlying PAN changes.

Enterprise merchants like Amazon consider tokenization essential, while another industry leader, JP Morgan, has discussed network tokenization as an “innovative approach to securing digital commerce.”

VGS is one of the few global players directly integrated with card networks to reduce latency and speed up processing. Network tokens from VGS are processor-agnostic but merchant-specific, expanding merchants' choices for payment vendors while containing their risk for fraud.

When merchants elect to store network tokens in VGS's independent vault over a PSP, they retain data ownership and facilitate processing redundancy for better payment outcomes. Processor-agnostic network tokens from VGS eliminate the dependency and operational inefficiency of processor-specific tokens held at individual PSPs. Merchants that control their network tokens can determine their processor instead of depending on their PSP. Merchants typically see 2-3%* higher authorization rates since fewer charges are declined due to outdated credentials. They can have 10 bps* lower processing costs since they receive pricing incentives with lower interchange rates from networks to adopt and use network tokens over PANs.

Account Updater

An account updater service enables merchants to keep their customers' card information accurate with updates. This is especially relevant for recurring subscriptions and in-the-moment purchases like on marketplaces or gig platforms. A rule of thumb is that 30-40% of cards change yearly due to scheduled updates and being lost, stolen, damaged, or otherwise reissued.

According to Visa, about 35% of customers forget to update their cards, so any time a merchant adds an account updater, they can expect that percentage of cards in their system to be updated. Due to account updaters, merchants face fewer declined transactions, while customers have a smoother experience that avoids unexpected service disruptions.

Although various providers - including PSPs, payment gateways, and networks - offer account update services, card updates are limited to those held by the PSP, facilitated by the gateways, or issued by that network.

Account updates from an independent vendor may have flexibility limitations. These can include updates that are always applied to all cards, including those that don't need to be updated. Or, cards are constantly updated even when the next transaction, such as an annual subscription fee, is months away.

Using the VGS Account Updater service enables merchants to hold their PAN without being liable for it on their systems. Merchants that own the PAN - over having it held by their PSP - can use it with the VGS Card Attributes service to obtain deeper card details that support better-architected loyalty and marketing programs, and share as needed with fraud and risk vendors.

VGS offers an industry-leading set of options on its account updater service. Besides receiving information on all their cards from a single provider, merchants can choose from in-the-moment and continuous updates in real-time, as well as select the cards in their database to which they'd like to apply the updates.

Combined Synergy for Successful Card Lifecycle Management

So if an account updater keeps merchants' customer payment details up to date and network tokens replace sensitive PANs with randomized tokens for smoother and safer payment processing…

Why Should You Use Both Account Updater and Network Tokens?

- Keep the PAN

- Maximum Coverage

- Automatic + Secure

- Cost Efficient

- A Complete Product Suite with Card Attributes

The flip side of replacing a PAN with a token is losing access to the PAN. Without the PAN, you have ceded control over your payment processing.

Let's consider a few scenarios here:

Examples include (not limited to):

- Retry Capability—Imagine that the PAN has changed. The merchant should not use it as is anymore, even if it's the same network token and the transaction is covered under the network token lifecycle. If the network token fails, you need the PAN to retry the transaction. An account updater is required to refresh the full PAN. Without the updated PAN and with just a failed network token, you simply cannot process that transaction.

- No PSP support—Imagine your PSP does not accept network tokens for processing, and the workaround offered by VGS for processors who don’t accept network tokens is not supported. Merchants will need the updated PAN for the PSP, which is available through account updater.

- Routing Choice—While global card networks offer rich data and security, reliance on network tokens can limit access to original PANs, hindering the ability to route transactions to local, cost-effective networks. Account updater allows the merchant to retain control over their network choice.

Although both services raise authorization rates differently, their combined effect furthers these.

For example, our account updater utilizes direct network API-based integration to get the latest updates, surpassing the industry standard of outdated batch file-based methods. Card information stays updated in real time and is more likely to result in a successful transaction.

While network tokens keep payment credentials current even when the PAN changes and receive pricing incentives for their use, merchants face a stumbling block:

Not all cards are network token-provisioned, and not all acquirer processors accept network tokens.

Scenario:

Take the example of a global QSR or fast food restaurant.

Their widespread presence will involve multiple PSPs who will likely have varying requirements and levels of support. They can prioritize security, fraud mitigation, and processing fee management with available network tokens. Account updater ensures they can offer a smooth user experience for payments made with cards-on-file in their app.

Both services combined cover the merchants across regions and PSPs while ensuring they are processing payments with the most current PAN, even when network tokens aren't available, to minimize friction and maximize retention.

If a merchant applies both services to the card information in their vault, the account updater ensures it stays current. Unique to VGS, merchants can choose from automatic continuous updates or updates as needed in real-time. Updates can be applied to all cards or a portion at any point before, during, or after the transaction. These card numbers can be replaced with processor-agnostic network tokens that stay updated even when the PAN number changes. The result is seamless updates that can be applied universally with no risk of fraudulent use, protecting both the merchant and their customers.

Scenario:

An example here could be any subscription service.

By using both, subscription service providers can refresh stored card data with an account updater, while network tokens protect that data, resulting in secure card data and uninterrupted payments.

Although both account updater and network token services are available from different providers, they are specific to that PSP, gateway, and network. If a merchant wanted to apply these services to all the cards in their database, partial coverage would be a hindrance. VGS-enabled services are neutral across providers, making it cost-effective to purchase these just once from a single vendor and get updates across all cards.

Scenario:

Take the instance of a large SaaS merchant.

They want to reduce their declined transactions and raise approval rates while minimizing the incidence of fraud on their millions of recurring payments. Rather than purchasing network tokens and account updater services multiple times, VGS offers agnostic solutions to merchants that enrich all their card data across networks and can be universally used across PSPs. A merchant can gain full control over network token provisioning and card account updates with interoperability to any end payment processor with a single vendor.

Access to the PAN isn't just helpful for successful card lifecycle management but also for going beyond that to better understand your customers and the cards they use.

We have previously written about VGS-enabled PAN Lookups offering more information on Card Attributes than BIN Lookups. Access to the Card Attributes equips merchants with an expanded information set and a bulwark against changing BIN requirements and incomplete information. But PAN Lookups aren't possible if the merchant doesn't even have a PAN.

Scenarios:

Changes to the card issuer, network, product, or other shifts

- Let's say the card portfolio has moved from Bank of America to Chase as the issuer, or there has been a network shift from Mastercard to Visa, or a card type change from credit to debit. With any of these shifts, the merchant could access more favorable pricing and other insights. But without an updated PAN, they can't leverage Card Attributes to pull the updates, like Chase now owning the BIN. The merchant is left with out-of-date information without an account updater and just a network token.

Changing BIN Requirements

- Visa and Mastercard mandated that after April 2022, any new BINs issued to issuing banks will be 8-digits due to a BIN shortage. If a card uses 8+ digit BINs, the existing 6-digit BIN lookup will return wrong or incomplete information.

- But once again, merchants who only have tokens and not the full PAN made available by the account updater service won't be able to use the information on their card attributes.

A complete product suite

- When VGS's Card Attributes, Network Tokens, and Account Updater are used together, merchants can use Card Attributes to review the BIN range and determine performance at a granular level. They can then implement that knowledge for better outcomes and decide whether to route payments with network tokens or a raw PAN. Still working with a single provider, merchants can use VGS Network Tokens and Account Updater to build out a robust payment strategy.

Both account updater and network tokens are critical to optimize card lifecycle management.

Forward-thinking merchants have a payment infrastructure that combines:

Control of their PAN and related insights

Coverage across PSPs, regions, products

Up-to-date information

Higher authorization rates

Cost efficiency

Friction-free user payment experiences

Continued security and PCI compliance

Pairing VGS's Account Updater and Network Tokens and adding on Card Attributes offers merchants all these.

You can access Network Tokens, Account Updater, and Card Attributes with a single API integration. The VGS Card Management Platform enables you to store and enrich all your payment data with one card object.

Learn More here.

Curious to know more about any of our products? Let's connect